Digitalisation of European countries: where are we at?

While we can’t really say technological innovation in finance is a recent phenomenon, there has been a great increase in investment in new technologies in recent years, with the pace of change now being exponential. In today's digital age, we have transitioned to a mobile-centric approach to banking, relying on advanced technology to facilitate our financial operations.

We handle payments, transfers, and investments using a variety of new tools that were not widely available a few years ago.

But not all businesses are doing well and, above all, not everywhere at equal pace.

European steps towards the digitalisation of businesses

The term “digital finance” is used to describe the impact of new technologies on the financial services industry. It encompasses a range of products, applications, processes, and business models that have revolutionised the delivery of banking and financial services.

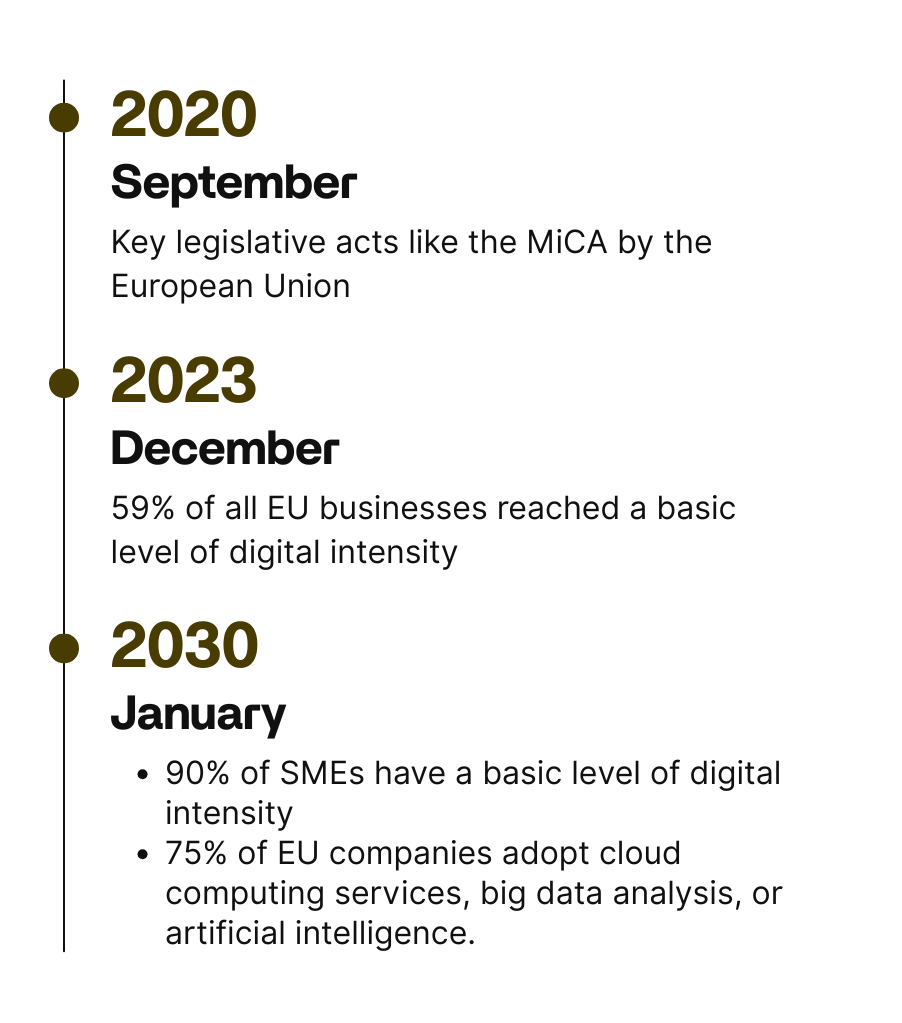

The EU Digital Finance Package is a strategic initiative aimed at enabling European market players to assume a leading role in the digital realm. As part of this push, the European Commission adopted a series of measures in September 2020. This initiative notably included key legislative acts like the MiCA, Markets in Crypto-Assets Regulation and set the stage for the revision of PSD3, the Payment Services Directive. These measures aim to support the digital transformation of financial services, while preserving stability and the integrity of the markets.

Overall, the EU has established two primary objectives for the digital transition of businesses by 2030, with the digitalisation of budgeting, payments, and cash-flow being a consistent part of this program.

By 2030, at least 90% of SMEs should have achieved a basic level of digital intensity and 75% of EU companies should adopt cloud computing services, big data analysis, or artificial intelligence. In 2023, 59% of all EU businesses reached a basic level of digital intensity. SMEs accounted for 58% of the total, which is around 32 percentage points below the EU 2030 target, while large businesses accounted for 91%.

The persistent digital gap between different countries and businesses

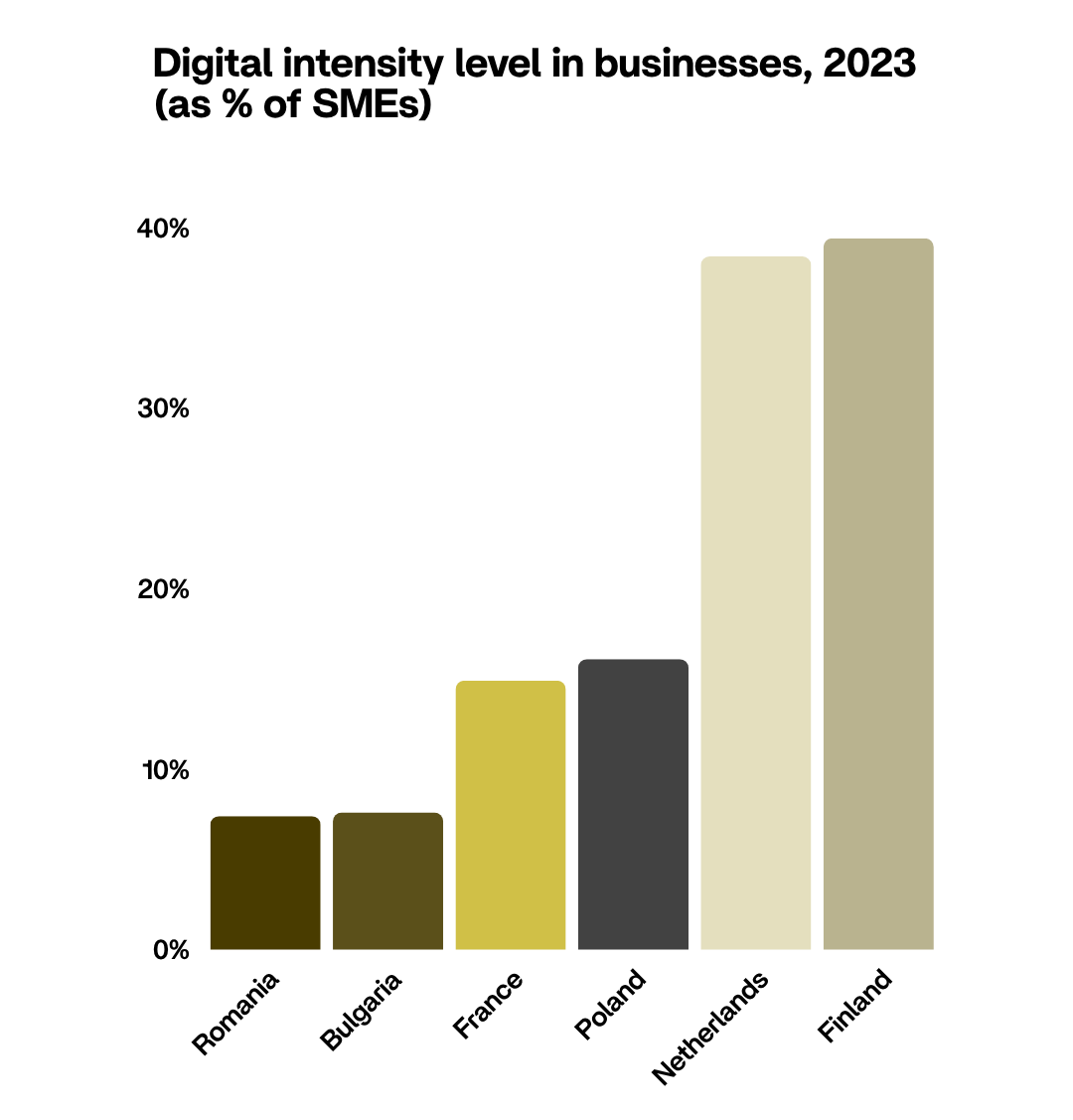

The proportion of SMEs with a high level of digital intensity ranged widely, from 7% in Romania and 8% in Bulgaria to 38% in the Netherlands and 39% in Finland.

This persistent gap is rooted in several critical barriers. Many SMEs cite the high initial cost of implementation, deepened by concerns over cybersecurity and the struggle to attract and retain talent with the necessary digital skills to manage complex, modern systems. For the 34% of businesses at the lowest intensity levels, digitalisation is often perceived as a prohibitive operational expense and not as a strategic investment.

The role of Generative AI

Use of digital financial services has also been recently simplified by advances in AI. Generative AI in particular is transforming areas like banking and insurance but also to simplify manual financial data filling. It is used in fraud detection, credit decisions, risk management, customer service, compliance, and portfolio management, improving accuracy and efficiency. AI is also being adopted in management and security, including trading and fluctuations analysis.

This push for AI integration is strongly supported by regional capabilities.

Poland, in particular, boasts deep expertise in software engineering, automation, and AI, accelerating investments across both public and private sectors. Recent initiatives include PLN 140 million for Poland’s fastest AI supercomputer in Kraków, PLN 200 million for a new AI factory in Poznań, and a PLN 300 million DeepTech Fund supporting innovation in cybersecurity, space technology, and artificial intelligence (Valians International, 2025).

Poland is fast emerging as Central and Eastern Europe's technology hub, with over 640.000 IT professionals (the largest tech talent pool in the region) (Valians International, 2025). Indeed, other European countries’ digital future is being held back by a significant SME deficit in optimizing the training of tech-skilled employees and finding specialists. Most SMEs externalise the tech-based services to multiple third parties, and let me tell you, when it comes to finance, better choose wisely.

The digital imperative in Poland

The data really leaves no doubt, many countries are not really keeping the pace of UE’s forecasts for small and medium enterprises. With 91% of large businesses already meeting the threshold, the challenge is about the equitable distribution of technology for SMEs.

The good news is that fintechs are playing an important part in setting a good example. In Poland, 2024 alone led venture capital funding to surpass EUR 800 million, with AI, fintech, and cybersecurity accounting for half of total investment (Valians International, 2025).

The national digitalisation of Poland was also the primary subject discussed at the Krajowa Izba Komunikacyjnej Ethernetowe (KIKE) 2025 conference.

Digital transformation has been adopted at an early stage by many companies in Central and Eastern Europe. However, Poland is ahead of other CEE countries : the use of e-invoices and e-tax declarations increased to 95%, and the issuance of e-prescriptions reached 2.3 billion in 2025.

Driving this transformation is the Digital Poland Program, which is set to run from 2021 to 2027, with a budget of over 3 billion USD. The program’s primary objectives are to enhance broadband coverage, strengthen cybersecurity, and expand digital public services, feeding an innovative environment.

While at this date Poland's level of SME digital intensity is aligned with the more global EU average due to the presence of highly digitised realities such as the Schengen area, it is proportionally increasing more and more every year. This serves as an example of how the challenges and opportunities of the European digital transition are played out on a national scale.

The core question to address here is what digitalisation actually means for finance and economics, and in the broader EU zone.

The summing up answer is that, while finance is doing well at keeping up with digital innovations, the precondition for any effort to make the financial field the driving force behind digital transformation in Europe, is a regulatory framework favourable to the fintech industry.

Webography

European Commission. (n.d.). Overview of digital finance. Retrieved December 2, 2025, from https://finance.ec.europa.eu/digital-finance/overview-digital-finance_en

Eurostat. (2024). Digitalisation in Europe – 2024 edition [Publication interactive]. https://ec.europa.eu/eurostat/web/interactive-publications/digitalisation-2024

Euronews. (2025, 3 novembre). Pologne: la numérisation de l'État, sujet principal de la conférence KIKE 2025. https://fr.euronews.com/2025/11/03/pologne-la-numerisation-de-letat-sujet-principal-de-la-conference-kike-2025

Valians International. (2026). POLAND IN MOTION: GROWTH DRIVERS 2026 [Livret numérique].

While we can’t really say technological innovation in finance is a recent phenomenon, there has been a great increase in investment in new technologies in recent years, with the pace of change now being exponential. In today's digital age, we have transitioned to a mobile-centric approach to banking, relying on advanced technology to facilitate our financial operations.

We handle payments, transfers, and investments using a variety of new tools that were not widely available a few years ago.

But not all businesses are doing well and, above all, not everywhere at equal pace.

European steps towards the digitalisation of businesses

The term “digital finance” is used to describe the impact of new technologies on the financial services industry. It encompasses a range of products, applications, processes, and business models that have revolutionised the delivery of banking and financial services.

The EU Digital Finance Package is a strategic initiative aimed at enabling European market players to assume a leading role in the digital realm. As part of this push, the European Commission adopted a series of measures in September 2020. This initiative notably included key legislative acts like the MiCA, Markets in Crypto-Assets Regulation and set the stage for the revision of PSD3, the Payment Services Directive. These measures aim to support the digital transformation of financial services, while preserving stability and the integrity of the markets.

Overall, the EU has established two primary objectives for the digital transition of businesses by 2030, with the digitalisation of budgeting, payments, and cash-flow being a consistent part of this program.

By 2030, at least 90% of SMEs should have achieved a basic level of digital intensity and 75% of EU companies should adopt cloud computing services, big data analysis, or artificial intelligence. In 2023, 59% of all EU businesses reached a basic level of digital intensity. SMEs accounted for 58% of the total, which is around 32 percentage points below the EU 2030 target, while large businesses accounted for 91%.

The persistent digital gap between different countries and businesses

The proportion of SMEs with a high level of digital intensity ranged widely, from 7% in Romania and 8% in Bulgaria to 38% in the Netherlands and 39% in Finland.

This persistent gap is rooted in several critical barriers. Many SMEs cite the high initial cost of implementation, deepened by concerns over cybersecurity and the struggle to attract and retain talent with the necessary digital skills to manage complex, modern systems. For the 34% of businesses at the lowest intensity levels, digitalisation is often perceived as a prohibitive operational expense and not as a strategic investment.

The role of Generative AI

Use of digital financial services has also been recently simplified by advances in AI. Generative AI in particular is transforming areas like banking and insurance but also to simplify manual financial data filling. It is used in fraud detection, credit decisions, risk management, customer service, compliance, and portfolio management, improving accuracy and efficiency. AI is also being adopted in management and security, including trading and fluctuations analysis.

This push for AI integration is strongly supported by regional capabilities.

Poland, in particular, boasts deep expertise in software engineering, automation, and AI, accelerating investments across both public and private sectors. Recent initiatives include PLN 140 million for Poland’s fastest AI supercomputer in Kraków, PLN 200 million for a new AI factory in Poznań, and a PLN 300 million DeepTech Fund supporting innovation in cybersecurity, space technology, and artificial intelligence (Valians International, 2025).

Poland is fast emerging as Central and Eastern Europe's technology hub, with over 640.000 IT professionals (the largest tech talent pool in the region) (Valians International, 2025). Indeed, other European countries’ digital future is being held back by a significant SME deficit in optimizing the training of tech-skilled employees and finding specialists. Most SMEs externalise the tech-based services to multiple third parties, and let me tell you, when it comes to finance, better choose wisely.

The digital imperative in Poland

The data really leaves no doubt, many countries are not really keeping the pace of UE’s forecasts for small and medium enterprises. With 91% of large businesses already meeting the threshold, the challenge is about the equitable distribution of technology for SMEs.

The good news is that fintechs are playing an important part in setting a good example. In Poland, 2024 alone led venture capital funding to surpass EUR 800 million, with AI, fintech, and cybersecurity accounting for half of total investment (Valians International, 2025).

The national digitalisation of Poland was also the primary subject discussed at the Krajowa Izba Komunikacyjnej Ethernetowe (KIKE) 2025 conference.

Digital transformation has been adopted at an early stage by many companies in Central and Eastern Europe. However, Poland is ahead of other CEE countries : the use of e-invoices and e-tax declarations increased to 95%, and the issuance of e-prescriptions reached 2.3 billion in 2025.

Driving this transformation is the Digital Poland Program, which is set to run from 2021 to 2027, with a budget of over 3 billion USD. The program’s primary objectives are to enhance broadband coverage, strengthen cybersecurity, and expand digital public services, feeding an innovative environment.

While at this date Poland's level of SME digital intensity is aligned with the more global EU average due to the presence of highly digitised realities such as the Schengen area, it is proportionally increasing more and more every year. This serves as an example of how the challenges and opportunities of the European digital transition are played out on a national scale.

The core question to address here is what digitalisation actually means for finance and economics, and in the broader EU zone.

The summing up answer is that, while finance is doing well at keeping up with digital innovations, the precondition for any effort to make the financial field the driving force behind digital transformation in Europe, is a regulatory framework favourable to the fintech industry.

Webography

European Commission. (n.d.). Overview of digital finance. Retrieved December 2, 2025, from https://finance.ec.europa.eu/digital-finance/overview-digital-finance_en

Eurostat. (2024). Digitalisation in Europe – 2024 edition [Publication interactive]. https://ec.europa.eu/eurostat/web/interactive-publications/digitalisation-2024

Euronews. (2025, 3 novembre). Pologne: la numérisation de l'État, sujet principal de la conférence KIKE 2025. https://fr.euronews.com/2025/11/03/pologne-la-numerisation-de-letat-sujet-principal-de-la-conference-kike-2025

Valians International. (2026). POLAND IN MOTION: GROWTH DRIVERS 2026 [Livret numérique].

Pour aller plus loin, découvrez nos derniers articles.

Vous y trouverez les recommandations de nos experts pour gérer vos opérations de commerce international de façon plus durable et responsable.

.jpg)

.jpg)

.jpg)