Who are the key fintech players? How to choose?

Too many fintech players are still competing on 2015 criteria. App ergonomics or the elimination of account opening fees. These aspects are now prerequisites. It's a mistake to consider them differentiators.

By 2026, any neobank can move funds in three clicks. Multi-currency payments, hedging, and risk management are no longer enough. A new front is emerging: impact.

But who are the main fintech players today? What are their strengths, and what are their weaknesses?

Let's take a look together.

Traditional Banks

The biggest players in finance, foreign exchange, and payments are traditional banks.

When businesses seek solutions for their active and modern operations, we must compare them. Traditional banks have experience and inspire confidence. They offer comprehensive and personalized services.

Their offerings often include all banking services: current accounts, savings accounts, loans, and investment solutions. They are less flexible for currency management and don't offer the advantage of a personal banking advisor, but they provide security and stability for savings, which remains a major asset. This can be reassuring for clients with complex financial needs, but not for those who prefer face-to-face interaction with an advisor.

However, traditional banks may charge higher fees for accounts, management, and international transactions. These fees may be justified by the diversity of services offered, but they can quickly add up for clients who don't take the time to carefully read all the footnotes.

In summary, immediate transparency is not their strong suit, nor is the often-lacking flexibility in their operations and services, despite recent improvements to the user experience (UX) aspects of their platforms. However, traditional banks rely on names established for decades, funding, and stock market listings, and not all the latest fintechs can claim the same scale.

A three-body problem: from Wise to Paygreen, via Revolut Business.

Today, the market is segmented into three distinct bodies around a single hub, at the crossroads of finance and technology.

Today's offerings generally differentiate themselves either by payment systems, innovations in the foreign exchange hedging sector, or other innovations that address contemporary issues, their problems, and their solutions. However, is there a platform that offers all three?

- Payment System Giants

This is where the battle for price, speed, and UX takes place. They are fast, inexpensive, and often feature very sleek platforms and apps.

Revolut Business

Revolut, in both its classic and Business versions, embodies the perfect plumbing. The best for solving a problem at the level of hic et nunc payment. Their platform benefits from ultra-fast logistical execution that resolves a transfer issue in three clicks. However, it's a system that doesn't often factor into the client's strategic thinking, especially long-term.

Everything is 100% automated, but is this automation truly limitless?

At Revolut, a critical weakness is the lack of human discernment. Their model relies on massive automation where the algorithm is the sole judge. As long as everything runs smoothly, the system is fluid. But as soon as a compliance block occurs, the customer faces a technological wall that doesn't always grasp the specifics of a business or the reality of a complex transaction.

Customer support becomes a dead end.

Wise

Wise is the leader in pricing transparency, eliminating hidden fees and displaying the real exchange rate. It's an excellent tool for managing everyday operations.

By opening an online Wise account, you can send money abroad, receive payments in other currencies, and make international expenditures. It is essentially a borderless account capable of managing multiple currencies. Registration is very simple, and it allows you to hold different currencies and convert them at the mid-market exchange rate.

The maximum transfer amount is set at $1,000,000 or the equivalent in your local currency. While this is of little importance for small businesses or freelancers, it somewhat limits the options for larger companies. Cost transparency does not guarantee compliance for all business types, nor does it provide support for risk management or overall strategy.

Their platform is designed for action, but not for the decision-making that precedes it.

- Foreign exchange players.

IbanFirst

IbanFirst offers technology focused on foreign exchange risk management, which is their core strength.

It offers reliable tools for managing cross-border transactions and margins. Its features include multi-currency accounts, real-time payment tracking, SWIFT transfers, free SEPA transfers, and access to forward contracts.

However, it does not offer integration with accounting or e-commerce platforms. Furthermore, businesses with an annual foreign exchange transaction volume of less than €200,000 will incur additional fees. For large businesses managing international payments, iBanFirst is a practical choice. However, it is not the most advantageous solution for small businesses, those dealing with only one currency, or those requiring integrations.

The added value stops at the barrier of traditional finance.

Convera

Formerly Western Union Business Solutions, Convera allows businesses to send and receive payments in 140 currencies across more than 200 countries. It represents the weighty legacy of traditional banks.

Convera offers forward contracts and allows for batch payments, but it lacks integrations with marketplaces and does not offer any credit or debit cards associated with its accounts.

Their model still largely relies on margin opacity, which is the exact opposite of the transparency needed to manage a modern business. Rates are not listed on the payment provider's website; they are only communicated after account creation.

This is a model that stumbles when faced with the need for clarity.

- The protagonists of impact and transition.

Shine

From an environmental perspective, Shine positions itself as a leading player in responsible finance, as demonstrated by its B Corp certification and its membership in the 1% for the Planet movement. These elements attest to a genuine and high-quality commitment to ethical and financial investment. Its strategy is based on a transparency policy that excludes fossil fuel financing, while providing entrepreneurs with measurable tools to calculate their carbon footprint.

However, its environmental strategy relies heavily on the concept of "offsetting," a term now considered obsolete, particularly through donating a fraction of its revenue. This may seem less transformative than a model where the banking transaction itself would directly act as a decarbonization lever with each transaction. Finally, its approach remains primarily focused on administrative management and awareness-raising, and sometimes lacks more advanced technical tools to thoroughly analyze the environmental impact of suppliers or the global supply chain of the companies it supports.

No real connection between financial operations and impact objectives.

PayGreen

PayGreen operates in the specific segment of online payments. Their solution allows businesses to collect payments while offering carbon offsetting tools or charitable round-ups at the time of purchase. It's an excellent entry point for e-commerce businesses looking to engage their end customers in a responsible approach. Here, the impact is directed towards the consumer and integrated into the payment process.

For an industrial SME or a mid-sized company, PayGreen does not address foreign exchange risk management or the optimization of global financial flows. It's an effective marketing and collection solution, but it does not constitute a complete financial infrastructure capable of managing all of a company's international operations.

In fact, that's not their primary objective.

Alternatives?

Keewe stands out as the only player capable of transforming a financial constraint into an impact driver by merging payment, hedging, and ecological and social transition within a single interface.

But that's not all.

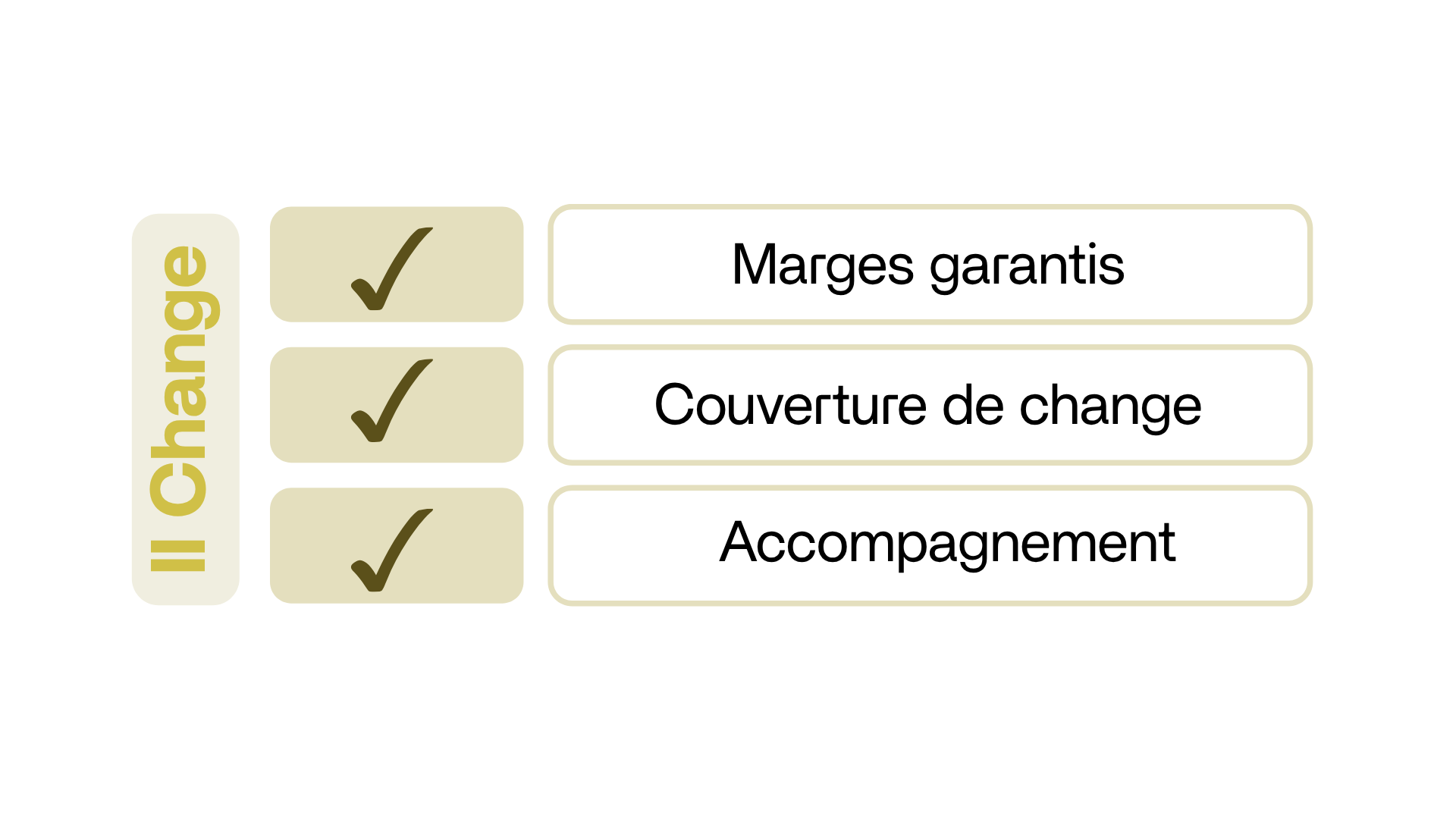

Where payment giants focus solely on execution and foreign exchange specialists on accounting techniques, Keewe influences the very trajectory of the company. By natively integrating the measurement and financing of the transition into the foreign exchange transaction, the platform enables companies to become major players in their CSR strategy, control and master foreign exchange risk, and manage their payments in over 200 currencies.

Keewe adopts a more operational strategy by integrating a Planet Dividend directly into the heart of its transactional model. This mechanism transforms each payment into a financial lever, enabling the decarbonization of the company's activity or the financing of transition projects, whereas competitors focus more on redistributing a portion of their revenues. Finally, Keewe stands out for its technical specialization in international flows and supplier analysis, thus offering a one-stop-shop solution for SMEs.

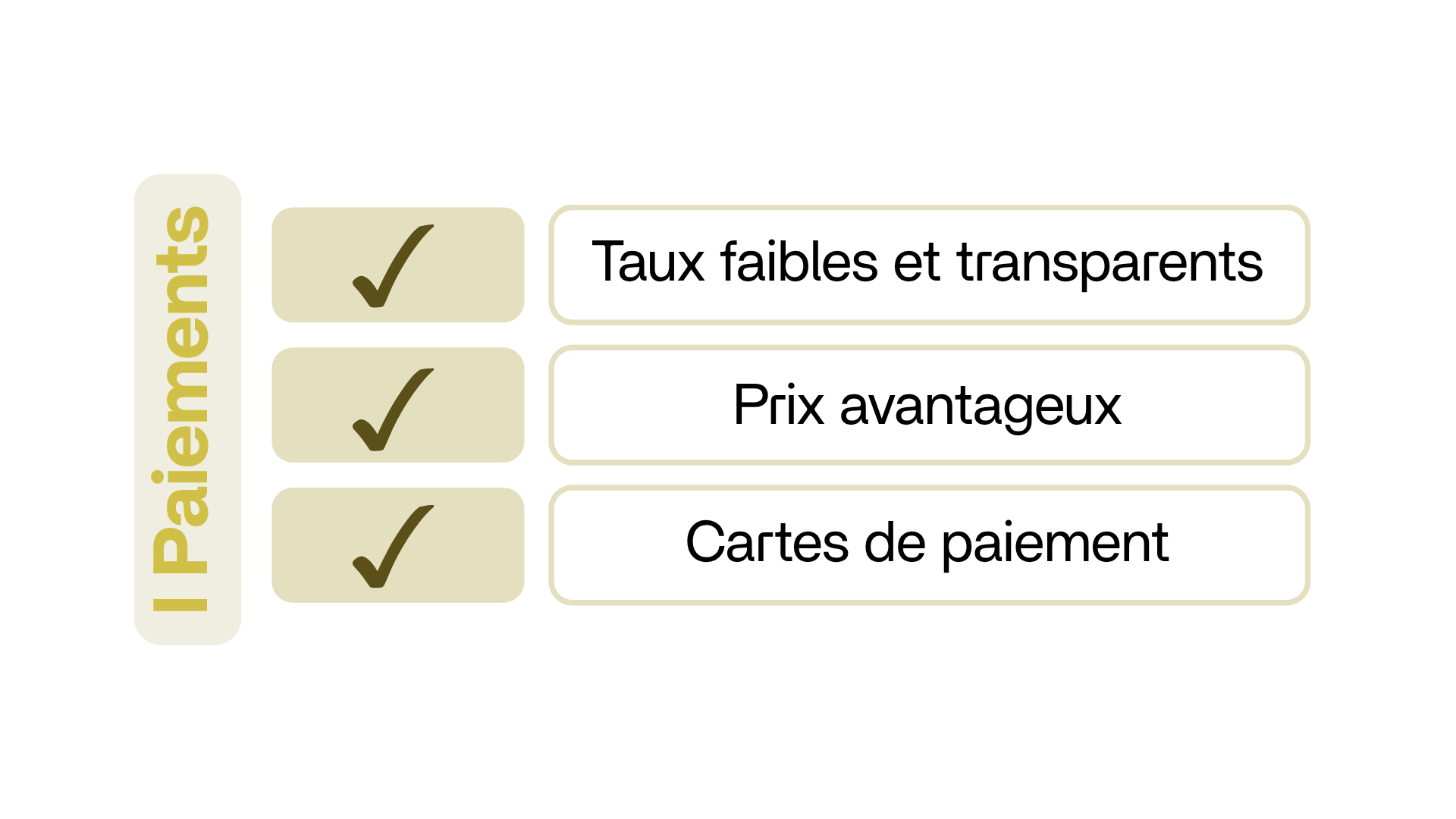

So, what's the added advantage? Impact is at the heart of every flow, integrated into payments while making them economical, transparent, and predictable, with guaranteed profit margins, thanks to expert support at every step.

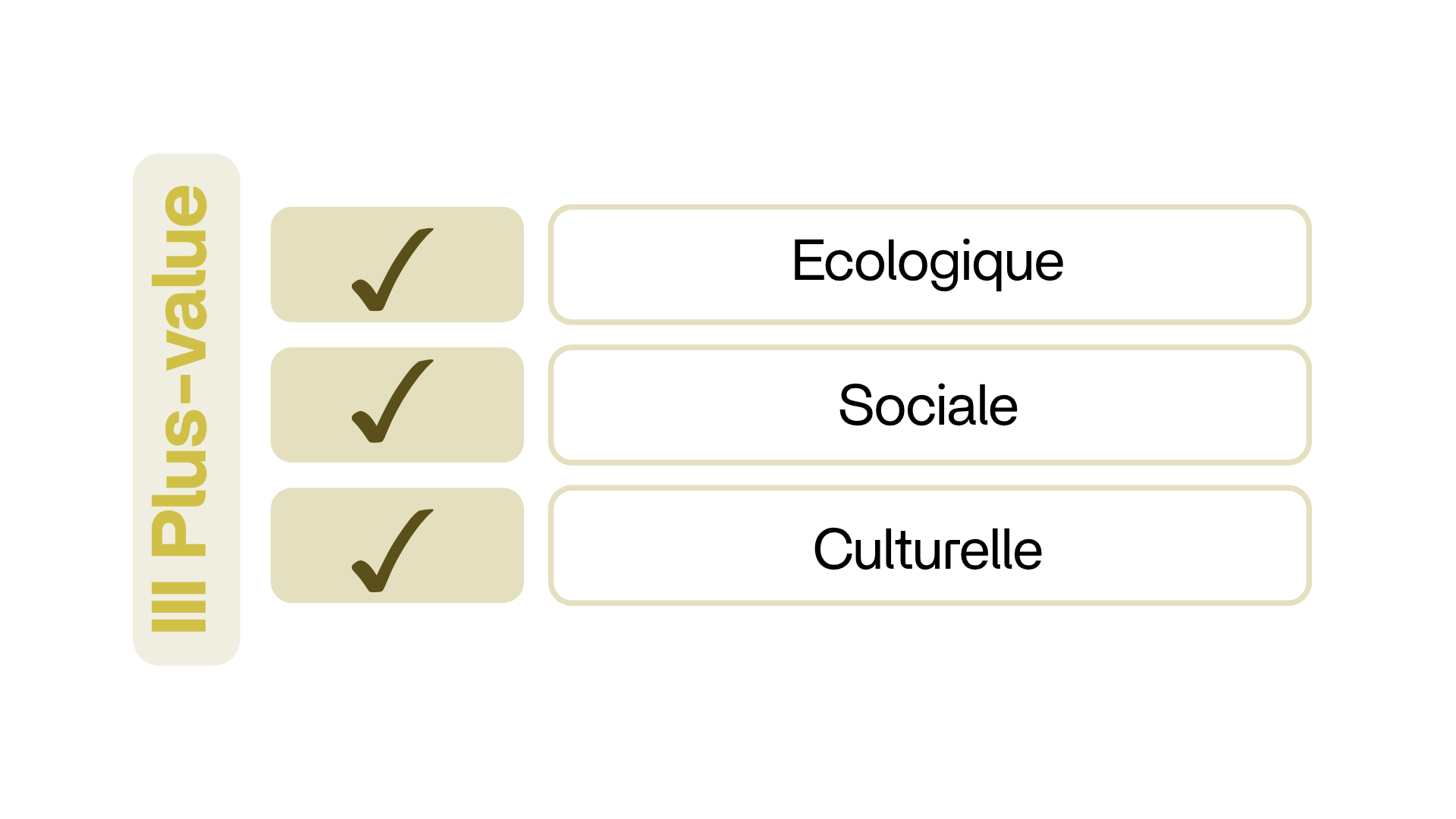

Keewe offers the transparency of Wise, the technical expertise of IbanFirst, the human discernment lacking in Revolut Business, and the ecological, social, and cultural added value of greentechs. It is the trusted partner that understands that the profitability and competitiveness of tomorrow's businesses are inseparable from today's responsibility.

Keewe creates the impact finance category.

To learn more about Keewe's offering, visit the page for Solutions or fill out our form for Contact 👇

We'd be happy to offer you the solution that best fits your needs.

Pour aller plus loin, découvrez nos derniers articles.

Vous y trouverez les recommandations de nos experts pour gérer vos opérations de commerce international de façon plus durable et responsable.

.jpg)

.jpg)

.jpg)

.jpg)